Houston Flood Insurance Costs: What Homeowners Need to Know in 2025

Do You Really Know What Determines Your Flood Insurance Cost?

Many Houston homeowners believe that flood insurance premiums are outrageously high or that they won’t qualify for coverage due to frequent flooding in the area.

However, this isn’t entirely true. A homeowner in The Woodlands expected to pay $2,000 per year for flood insurance—but after reviewing the right factors, their actual cost was closer to $800. So, what determines your flood insurance premium in Houston?

By the end of this article, you’ll understand:

-The real cost of flood insurance in Houston

–How Houston’s geography impacts your rates

-How to reduce your premium

-When to choose NFIP vs. private flood insurance

Many Houston homeowners believe that flood insurance premiums are outrageously high or that they won’t qualify for coverage due to frequent flooding in the area.

However, this isn’t entirely true.

A homeowner in The Woodlands expected to pay $2,000 per year for flood insurance—but after reviewing the right factors, their actual cost was closer to $800.

So, what actually determines your flood insurance premium in Houston?

By the end of this article, you’ll understand:

Many Houston homeowners believe that flood insurance premiums are outrageously high or that they won’t qualify for coverage due to frequent flooding in the area.

However, this isn’t entirely true.

A homeowner in The Woodlands expected to pay $2,000 per year for flood insurance—but after reviewing the right factors, their actual cost was closer to $800.

So, what actually determines your flood insurance premium in Houston?

By the end of this article, you’ll understand:

How Much Does Flood Insurance Cost in Houston?

The Average Premium Range

The average flood insurance premium in Houston typically ranges from $1,500 to $2,000 per year. However, prices vary significantly based on multiple factors.

Some homeowners pay as little as $800 per year, while others pay over $3,000 due to their home’s unique risk profile.

What Factors Impact Your Flood Insurance Cost?

Flood zones used to be the biggest factor in pricing, but with FEMA’s Risk Rating 2.0, your premium now depends on:

Elevation – Homes built above the Base Flood Elevation (BFE) typically have lower premiums.

Proximity to reservoirs and bayous – The closer your home is to a major water source, the higher your risk.

Floodproofing and mitigation – Features like flood vents, grading, and drainage improvements can reduce premiums.

Past flood claims – If your home has flooded in the last five years, you may pay a higher premium.

How Risk Rating 2.0 Changed Houston’s Flood Insurance Pricing

FEMA’s Risk Rating 2.0 introduced a new pricing model that no longer uses flood zones as the primary factor. Instead, it considers:

Distance to water sources

Elevation differences

Historical flooding patterns

Home construction type and materials

How to Lower Your Flood Insurance Premium in Houston

1. Get an Elevation Certificate

An Elevation Certificate (EC) helps determine if your home is above Base Flood Elevation (BFE). If it is, you may qualify for lower rates.

2. Improve Flood Protection Measures

Insurers offer discounts for homes with:

–Flood vents to relieve hydrostatic pressure

–Sump pumps to prevent basement flooding

–Proper drainage systems to divert water away

3. Compare at Least Three Flood Insurance Quotes Each Year

Many Houston homeowners only look at NFIP rates. Instead, you should:

✔ Compare at least three private flood insurance providers

✔ Ask about flood mitigation discounts

✔ Review your policy annually for the best rates

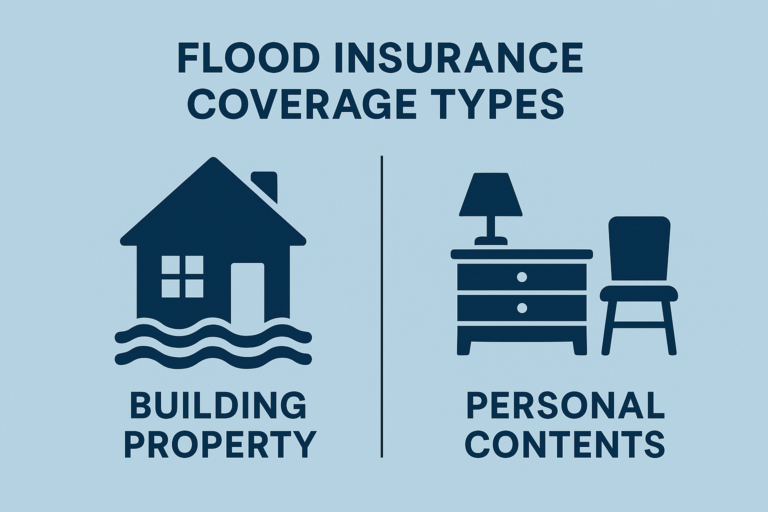

NFIP vs. Private Flood Insurance: Which Is Better for Houston Homeowners?

1. National Flood Insurance Program (NFIP)

- Backed by FEMA

- Covers up to $250,000 for home + $100,000 for contents

- Rates may be lower in high-risk areas due to subsidies

2. Private Flood Insurance

- Higher coverage limits (ideal for homes above $250,000)

- Covers additional living expenses and replacement cost for contents

Can be cheaper than NFIP in some areas

Common Misconceptions About Flood Insurance in Houston

Myth 1: “Flood insurance is too expensive

Reality: Many policies start at $800 per year, depending on your home’s risk factors.

Myth 2: “The NFIP is my only option.”

➡ Learn More:

Reality: Many homeowners qualify for private flood insurance, which may offer better coverage at lower rates.

Myth 3: “I only need coverage for my mortgage balance.”

Reality: Your mortgage lender requires minimum coverage, but this may not be enough to rebuild after a major flood.

Final Thoughts: What’s Next?

Let me call him real quick-Compare Private & NFIP Quotes to find the best price

He’s really busy

Now that you understand how flood insurance rates are determined, it’s time to take action:

Navigating the Waters of Flood Insurance in COBRA Zones

When it comes to protecting your home from the unpredictable forces of nature, understanding your flood insurance options is crucial. Many homeowners find themselves navigating the complex landscape of flood insurance, especially when their property lies within a COBRA zone. You’ve asked, and we’re here to answer all your pressing questions about flood insurance in these unique areas.

What Exactly is a COBRA Zone?

What makes COBRA zones different from other flood zones, and why does it matter for my flood insurance?

COBRA zones, or Coastal Barrier Resources System areas, are designated by the federal government to protect natural coastal barriers. Development in these zones is discouraged to conserve natural habitats, minimize loss of human life, and reduce federal expenditure on infrastructure and disaster relief. For homeowners, this means that obtaining federal flood insurance through the National Flood Insurance Program (NFIP) is not an option, making it essential to explore alternative insurance solutions.

Can I Get Flood Insurance in a COBRA Zone?

They Ask: If federal flood insurance isn’t available in COBRA zones, what are my options for protecting my property?

You Answer: While properties in COBRA zones are ineligible for federal flood insurance, private flood insurance becomes a vital alternative. Private insurers offer policies designed to meet the unique needs of homeowners in these areas, ensuring you can secure the protection you need against flooding. It’s crucial to work with an insurance agent who understands the intricacies of flood insurance policies in COBRA zones to find the best coverage for your home.

How Do I Know If My Property is in a COBRA Zone?

They Ask: How can I determine if my property is located within a COBRA zone and understand the implications for my flood insurance coverage?

You Answer: Identifying whether your property is in a COBRA zone is the first step in navigating your flood insurance options. You can use tools like the CBRS Mapper provided by the Fish and Wildlife Service or consult with a knowledgeable insurance agent. Understanding your property’s location helps clarify your insurance options and ensures you’re pursuing the right coverage for your situation.

What Should I Look for in a Flood Insurance Policy?

They Ask: What key factors should I consider when choosing a flood insurance policy for my property in a COBRA zone?

You Answer: When selecting a flood insurance policy in a COBRA zone, consider coverage limits, deductibles, and exclusions. It’s also important to assess the insurer’s reputation and the policy’s provisions for claims handling. An insurance agent specializing in flood insurance can help you compare policies and choose one that offers comprehensive protection tailored to your needs.

Conclusion

Understanding flood insurance in COBRA zones doesn’t have to be a daunting task. By asking the right questions and seeking expert advice, you can navigate the complexities of securing the right flood insurance for your property. Remember, protecting your home from flooding is about ensuring your peace of mind and financial security, regardless of where you live.

Navigating the Waters of Flood Insurance in COBRA Zones

When it comes to protecting your home from the unpredictable forces of nature, understanding your flood insurance options is crucial. Many homeowners find themselves navigating the complex landscape of flood insurance, especially when their property lies within a COBRA zone. You’ve asked, and we’re here to answer all your pressing questions about flood insurance in these unique areas.

What Exactly is a COBRA Zone?

What makes COBRA zones different from other flood zones, and why does it matter for my flood insurance?

COBRA zones, or Coastal Barrier Resources System areas, are designated by the federal government to protect natural coastal barriers. Development in these zones is discouraged to conserve natural habitats, minimize loss of human life, and reduce federal expenditure on infrastructure and disaster relief. For homeowners, this means that obtaining federal flood insurance through the National Flood Insurance Program (NFIP) is not an option, making it essential to explore alternative insurance solutions.

Can I Get Flood Insurance in a COBRA Zone?

They Ask: If federal flood insurance isn’t available in COBRA zones, what are my options for protecting my property?

You Answer: While properties in COBRA zones are ineligible for federal flood insurance, private flood insurance becomes a vital alternative. Private insurers offer policies designed to meet the unique needs of homeowners in these areas, ensuring you can secure the protection you need against flooding. It’s crucial to work with an insurance agent who understands the intricacies of flood insurance policies in COBRA zones to find the best coverage for your home.

How Do I Know If My Property is in a COBRA Zone?

They Ask: How can I determine if my property is located within a COBRA zone and understand the implications for my flood insurance coverage?

You Answer: Identifying whether your property is in a COBRA zone is the first step in navigating your flood insurance options. You can use tools like the CBRS Mapper provided by the Fish and Wildlife Service or consult with a knowledgeable insurance agent. Understanding your property’s location helps clarify your insurance options and ensures you’re pursuing the right coverage for your situation.

What Should I Look for in a Flood Insurance Policy?

They Ask: What key factors should I consider when choosing a flood insurance policy for my property in a COBRA zone?

You Answer: When selecting a flood insurance policy in a COBRA zone, consider coverage limits, deductibles, and exclusions. It’s also important to assess the insurer’s reputation and the policy’s provisions for claims handling. An insurance agent specializing in flood insurance can help you compare policies and choose one that offers comprehensive protection tailored to your needs.

Conclusion

Understanding flood insurance in COBRA zones doesn’t have to be a daunting task. By asking the right questions and seeking expert advice, you can navigate the complexities of securing the right flood insurance for your property. Remember, protecting your home from flooding is about ensuring your peace of mind and financial security, regardless of where you live.

Navigating the Waters of Flood Insurance in COBRA Zones

When it comes to protecting your home from the unpredictable forces of nature, understanding your flood insurance options is crucial. Many homeowners find themselves navigating the complex landscape of flood insurance, especially when their property lies within a COBRA zone. You’ve asked, and we’re here to answer all your pressing questions about flood insurance in these unique areas.

What Exactly is a COBRA Zone?

What makes COBRA zones different from other flood zones, and why does it matter for my flood insurance?

COBRA zones, or Coastal Barrier Resources System areas, are designated by the federal government to protect natural coastal barriers. Development in these zones is discouraged to conserve natural habitats, minimize loss of human life, and reduce federal expenditure on infrastructure and disaster relief. For homeowners, this means that obtaining federal flood insurance through the National Flood Insurance Program (NFIP) is not an option, making it essential to explore alternative insurance solutions.

Can I Get Flood Insurance in a COBRA Zone?

They Ask: If federal flood insurance isn’t available in COBRA zones, what are my options for protecting my property?

You Answer: While properties in COBRA zones are ineligible for federal flood insurance, private flood insurance becomes a vital alternative. Private insurers offer policies designed to meet the unique needs of homeowners in these areas, ensuring you can secure the protection you need against flooding. It’s crucial to work with an insurance agent who understands the intricacies of flood insurance policies in COBRA zones to find the best coverage for your home.

How Do I Know If My Property is in a COBRA Zone?

They Ask: How can I determine if my property is located within a COBRA zone and understand the implications for my flood insurance coverage?

You Answer: Identifying whether your property is in a COBRA zone is the first step in navigating your flood insurance options. You can use tools like the CBRS Mapper provided by the Fish and Wildlife Service or consult with a knowledgeable insurance agent. Understanding your property’s location helps clarify your insurance options and ensures you’re pursuing the right coverage for your situation.

What Should I Look for in a Flood Insurance Policy?

They Ask: What key factors should I consider when choosing a flood insurance policy for my property in a COBRA zone?

You Answer: When selecting a flood insurance policy in a COBRA zone, consider coverage limits, deductibles, and exclusions. It’s also important to assess the insurer’s reputation and the policy’s provisions for claims handling. An insurance agent specializing in flood insurance can help you compare policies and choose one that offers comprehensive protection tailored to your needs.

Conclusion

Understanding flood insurance in COBRA zones doesn’t have to be a daunting task. By asking the right questions and seeking expert advice, you can navigate the complexities of securing the right flood insurance for your property. Remember, protecting your home from flooding is about ensuring your peace of mind and financial security, regardless of where you live.

Navigating the Waters of Flood Insurance in COBRA Zones

When it comes to protecting your home from the unpredictable forces of nature, understanding your flood insurance options is crucial. Many homeowners find themselves navigating the complex landscape of flood insurance, especially when their property lies within a COBRA zone. You’ve asked, and we’re here to answer all your pressing questions about flood insurance in these unique areas.

What Exactly is a COBRA Zone?

What makes COBRA zones different from other flood zones, and why does it matter for my flood insurance?

COBRA zones, or Coastal Barrier Resources System areas, are designated by the federal government to protect natural coastal barriers. Development in these zones is discouraged to conserve natural habitats, minimize loss of human life, and reduce federal expenditure on infrastructure and disaster relief. For homeowners, this means that obtaining federal flood insurance through the National Flood Insurance Program (NFIP) is not an option, making it essential to explore alternative insurance solutions.

Can I Get Flood Insurance in a COBRA Zone?

They Ask: If federal flood insurance isn’t available in COBRA zones, what are my options for protecting my property?

You Answer: While properties in COBRA zones are ineligible for federal flood insurance, private flood insurance becomes a vital alternative. Private insurers offer policies designed to meet the unique needs of homeowners in these areas, ensuring you can secure the protection you need against flooding. It’s crucial to work with an insurance agent who understands the intricacies of flood insurance policies in COBRA zones to find the best coverage for your home.

How Do I Know If My Property is in a COBRA Zone?

They Ask: How can I determine if my property is located within a COBRA zone and understand the implications for my flood insurance coverage?

You Answer: Identifying whether your property is in a COBRA zone is the first step in navigating your flood insurance options. You can use tools like the CBRS Mapper provided by the Fish and Wildlife Service or consult with a knowledgeable insurance agent. Understanding your property’s location helps clarify your insurance options and ensures you’re pursuing the right coverage for your situation.

What Should I Look for in a Flood Insurance Policy?

They Ask: What key factors should I consider when choosing a flood insurance policy for my property in a COBRA zone?

You Answer: When selecting a flood insurance policy in a COBRA zone, consider coverage limits, deductibles, and exclusions. It’s also important to assess the insurer’s reputation and the policy’s provisions for claims handling. An insurance agent specializing in flood insurance can help you compare policies and choose one that offers comprehensive protection tailored to your needs.

Conclusion

Understanding flood insurance in COBRA zones doesn’t have to be a daunting task. By asking the right questions and seeking expert advice, you can navigate the complexities of securing the right flood insurance for your property. Remember, protecting your home from flooding is about ensuring your peace of mind and financial security, regardless of where you live.

Information contained on this page is provided by an independent third-party content provider. This website make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact editor @producerpress.com