Ohio Valley Flooding: What Homeowners and Business Owners Should Do Next

What to Do After Flood Damage: A Step-by-Step Guide for Ohio Valley Homeowners and Business Owners

Has your home or business in the Ohio Valley area — including parts of Kentucky, Indiana, or Ohio — been impacted by recent severe flooding?

Are you feeling overwhelmed and unsure what to do first, especially when it comes to filing your insurance claim?

You’re not alone. Flood damage can be devastating, both physically and emotionally — and navigating the insurance process during a regional disaster only adds to the stress. But there are clear steps you can take to protect your property, avoid costly mistakes, and make sure you get what you’re owed.

In this article, we’ll guide you through what to do immediately after flood damage, how to deal with your insurance company, how flood coverage actually works, and what to expect if you’ve already filed a claim this year.

First Steps to Take Immediately After Flood Damage

Safety is your top priority. If you haven’t already, make sure everyone is safe and that the property is no longer in active danger (e.g., rising water, electrical hazards, structural damage).

Once safe, here’s what to do next:

– Document everything: Take detailed photos and videos of every affected room, damaged items, water lines on walls, debris, and anything that’s no longer functional.

– Don’t throw anything away yet: Your insurance adjuster needs to see the damage. If something must be discarded for safety reasons, photograph it from every angle first.

– Create a loss inventory: List all damaged items with brand names, models, estimated value, and date of purchase if possible.

– Prevent further damage: If you can safely remove water or place tarps, do so — but don’t begin full cleanup or repairs until the adjuster has seen the damage.

What Your Insurance Company Needs From You

The sooner you contact your insurance company, the better. Claims are already backing up across counties in Kentucky, Indiana, and Ohio. Early contact helps lock in your place in the adjuster queue — but you still need to follow the formal claim process correctly.

Most flood insurance policies — including those backed by the National Flood Insurance Program (NFIP) — require a Proof of Loss form to be submitted within 60 days of the flood. This form documents what was damaged and how much you’re claiming in losses.

> If you miss the 60-day window, your claim can be denied — even if you’ve already spoken to your insurer or had an adjuster visit. Don’t assume verbal communication is enough. File in writing.

Understanding Flood Insurance Coverage, Deductibles, and What “Flood Damage” Really Means

If you’re navigating flood damage for the first time — or even if it’s your second time — understanding what’s actually covered (and what isn’t) is critical.

Don’t Be Caught Off Guard by the Deductible

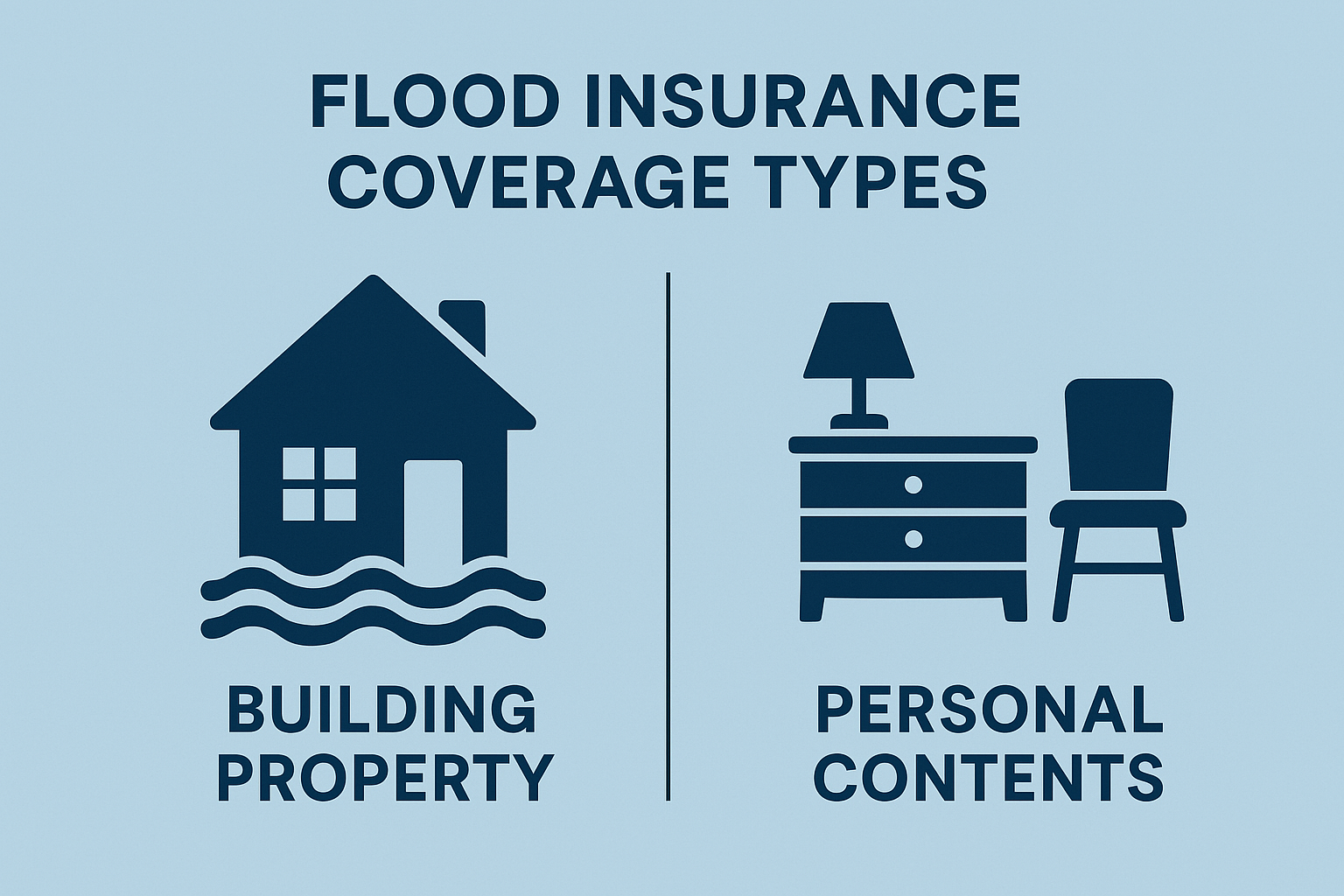

Every coverage type in a flood policy has its own separate deductible.

Most flood policies split into:

1. Building Property Coverage – for the structure of your home or business

2. Personal Property (Contents) Coverage – for your belongings

> If you have $1,000 deductibles for both, that means you’re responsible for the first $1,000 of damage to the structure and the first $1,000 of damage to your contents — not just one combined amount.

Homeowners Insurance Doesn’t Cover Flooding

> Standard homeowners policies in Ohio, Kentucky, and Indiana do not cover flood damage.

You must have a separate flood policy — through the NFIP or a private insurer — to receive coverage.

What Is Considered “Flood Damage”?

To qualify as a “flood” under most policies, the damage must result from **water affecting two or more acres or two or more properties.** Common qualifying events include:

– Overflowing rivers or creeks

– Flash floods or surface water accumulation

– Groundwater entering due to rising outside water levels

– Mudflow caused by heavy rains

Damage from burst pipes, roof leaks, or sewer backups is usually not covered under flood insurance.

> Tip: The cause of the water is what matters. Document everything and ask your adjuster to clarify coverage in writing.

What If This Is Your Second Flood Claim This Year?

With back-to-back storms in the Ohio Valley, many property owners are filing a second claim within the same policy year. Here’s what to know:

–

So if your building coverage is $250,000 and you receive $200,000 from one flood event, you could still receive up to another $250,000 for a second, unrelated flood loss, as long as it’s a new covered flood event and your policy is still in force. The only time the total limit across events becomes a hard cap is when dealing with:

• Duplicate policies (like RCBAP + Dwelling Form on the same unit),

• Repetitive Loss or ICC payouts, or

• A single event claim exhausting the limits.

– Private flood insurance generally allows multiple claims as long as the policy is active at the time of the loss.

– Even if you’ve been sent a non-renewal notice, you are typically covered up until that expiration date.

> Every private flood insurance policy is different. While most will still cover you as long as the policy is in force on the date of loss, you should confirm this directly with your insurance provider. Coverage limits, deductibles, and per-claim allowances vary.

–

–

Local Flood Resources in the Ohio Valley Region

Here are trusted sources for help and information:

– [FEMA Disaster Assistance](https://www.disasterassistance.gov)

– [Ohio Insurance Department](https://insurance.ohio.gov)

– [Kentucky Department of Insurance](https://insurance.ky.gov)

– [Indiana Department of Insurance](https://www.in.gov/idoi/)

– [American Red Cross Flood Help](https://www.redcross.org/get-help.html)

How to Prepare for Next Time

Flooding is increasingly common — even in areas not previously considered high risk. Here’s how to reduce risk and protect your investment going forward:

– Review your flood policy annually

– Understand basement limitations: Most policies offer limited or no coverage for drywall, flooring, and contents in finished basements

– Ask your agent about add-ons or excess coverage

– Store valuables in waterproof containers or move them above ground level

Final Thoughts: You’re Not Alone — and You’re Not Powerless

Flood damage is overwhelming — emotionally, physically, and financially. But now that you know what to do first, how to document everything, and what your insurance is (and isn’t) likely to cover, you’re far better prepared to protect yourself.

If you still have questions or feel unsure about your coverage, the worst thing you can do is wait.

At The Flood Insurance Guru, we help property owners in the Ohio Valley understand their flood insurance, maximize their claims, and avoid costly surprises. No pressure — just real answers.

Information contained on this page is provided by an independent third-party content provider. This website make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact editor @producerpress.com