Flood Insurance for Connecticut Multi-Family Properties: Essential Guide

The $150,000 Mistake That Cost One Investor Everything

You did everything right. You bought a six-unit building in Hartford, insured it for what your lender required, and your rental income was steady.

Then the flood hit.

The damage totaled $650,000. Your policy only covered $500,000. Your tenants were out for eight months, and so was your income. You ended up $150,000 short on repairs and $60,000 down in lost rent, forced to borrow just to recover.

In this guide, I’ll show you the key differences between 1 to 4 unit and 5 or more unit flood insurance, the three costly coverage gaps, and how to protect your rental income before the next storm hits.

1-4 Unit Properties: Residential Classification

If you own a duplex, triplex, or fourplex in Connecticut, your property is classified as residential for flood insurance purposes. This means:

-

Bank Requirement: Typically $250,000 in building coverage

-

NFIP Maximum: $250,000 building / $100,000 contents

-

Contents Coverage: Personal property only (tenant belongings not covered by your policy)

-

Loss of Rental Income: Not typically required by lenders, often not included

5+ Unit Properties: Commercial Classification

Once you own a property with five or more units, everything changes. Your building is now classified as commercial or non-residential. This means:

-

Bank Requirement: Typically $500,000 in building coverage

-

NFIP Maximum: $500,000 building / $500,000 contents

-

Contents Coverage: Business personal property (appliances, HVAC, common area furnishings)

-

Loss of Rental Income: Available but not automatically included

Flood insurance premiums for Connecticut properties with five or more units typically range from $5,000 to $10,000 per year for standard $500,000 building coverage. Adding contents and rental income coverage increases costs by 20 to 30 percent, bringing the annual total to approximately $6,000 to $13,000 per building.

The Three Coverage Gaps That Destroy Multi-Family Investors

Gap #1: The Bank Minimum Trap

Your lender requires $500,000 in flood insurance. You comply. But your six-unit apartment building in New Haven costs $800,000 to rebuild. A major flood causes $700,000 in damage. Your policy pays out only $500,000. You’re left with a $200,000 shortfall, plus costs for tenant displacement and reconstruction.

The solution: Always insure to full replacement cost. If your building would cost $800,000 to rebuild, that’s how much coverage you need, regardless of what your lender requires. Private carriers can exceed NFIP limits.

Gap #2: The Loss of Rental Income Blindspot

A flood disables your property for eight months. You’re collecting no rent, but your mortgage, taxes, and insurance still come due. If you earn $2,500 per unit, that’s $120,000 in lost income.

The solution: Add loss of rental income coverage to your policy. This coverage typically adds 20 to 30 percent to your premium but can save you from financial ruin during major flood repairs.

Gap #3: The Business Contents Confusion

Your six-unit building contains:

-

Six HVAC units ($30,000)

-

Six water heaters ($6,000)

-

Refrigerators and stoves ($12,000)

-

Furnishings and laundry equipment ($13,000)

That’s $61,000 in business contents that won’t be covered unless your policy includes this specific protection.

The solution: Add business contents coverage. I recommend $50,000 to $100,000 depending on the size and equipment in your building.

Real Cost of Flood Insurance for Connecticut Multi-Family Properties

Baseline Coverage: $500,000 Building Only

-

Premium: $5,000 to $10,000 annually

-

Flood Zone Impact: Minimal for NFIP, significant for private

Comprehensive Coverage: Building + Contents + Rental Income

-

Premium: $6,000 to $13,000 annually

-

Add-on Costs: Contents +10 to 15 percent, Rental Income +10 to 15 percent

-

Total Increase: 20 to 30 percent over baseline

The Lender Requirement Confusion

What Banks Require

-

Coverage up to loan balance or NFIP max

-

Proof of coverage

-

No lapses

What Banks Don’t Require (But You Need)

-

Full replacement value coverage

-

Rental income protection

-

Business contents coverage

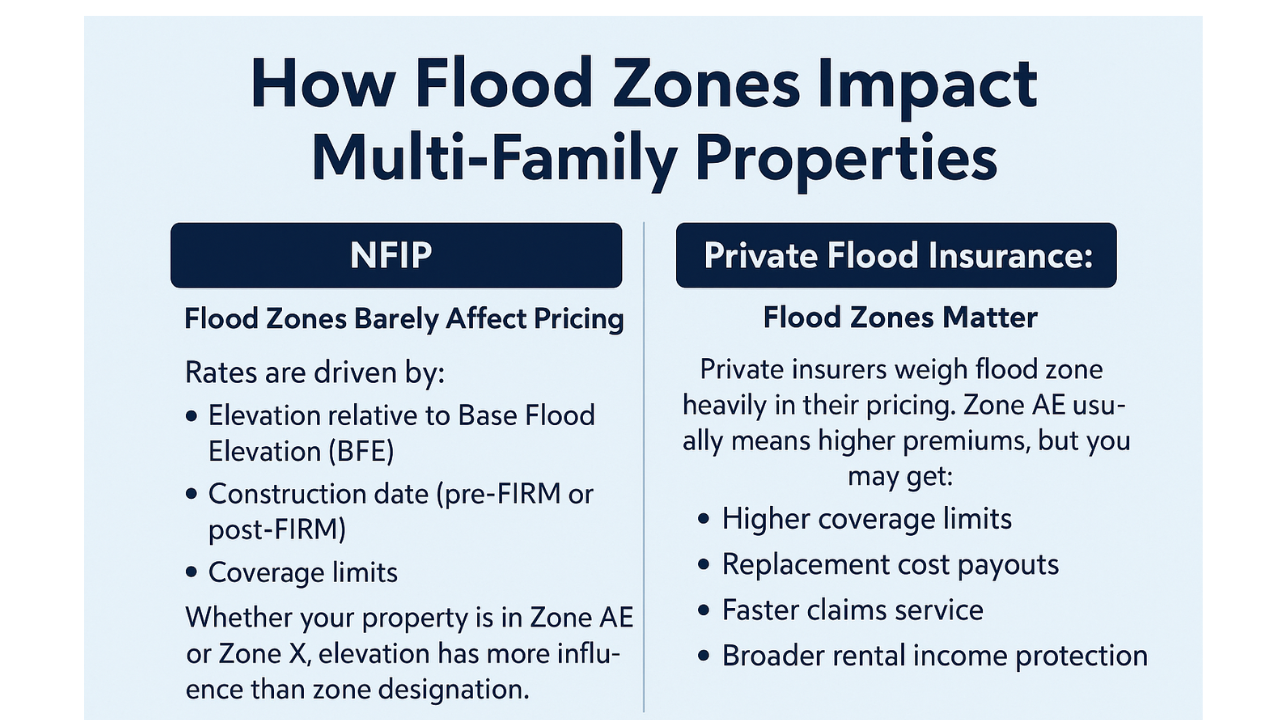

NFIP vs. Private Insurance for Multi-Family Properties

When NFIP May Be Right

-

Building value under $500,000

-

Located in moderate-risk zone

-

No need for rental income coverage

When Private Insurance Is Better

-

Building value exceeds $500,000

-

Need for rental income and contents coverage

-

Desire for replacement cost and better claims service

The Hybrid Strategy

Some investors layer coverage by:

-

Using NFIP for the base $500,000

-

Adding private excess coverage

-

Using private for rental income and contents protection

FAQ About Flood Insurance for Multi-Family Properties

Do I need flood insurance for a duplex in Connecticut?

Yes, if you’re in a designated flood zone and have a mortgage. Even in lower-risk areas, flood coverage is strongly advised. Most duplexes exceed the NFIP’s $250,000 limit, so private insurance is often necessary.

What’s the difference between a 4-unit and 6-unit property?

A 4-unit is residential and capped at $250,000 coverage. A 6-unit is commercial with access to $500,000 NFIP coverage and better private options. Pricing and flexibility both increase.

Does flood insurance cover lost rental income?

Only if you add that coverage. NFIP does not include it by default. Private insurers offer it as an endorsement. I recommend 12 months of rental income protection for all investors.

Can I get more than $500,000 in coverage?

Yes, through private carriers. Many offer $1 to $2 million in building coverage, plus contents and rental income options. Expect to pay $12,000 to $18,000 annually for full protection on high-value properties.

Don’t Let Bank Minimums Destroy Your Investment

You’ve worked hard to build your rental portfolio. Don’t let an incomplete flood policy undo it all.

We’ll assess your current policy and show you how to close any gaps.

Don’t wait until it’s too late. Protect your income, your investment, and your future.

Information contained on this page is provided by an independent third-party content provider. This website make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact editor @producerpress.com