Does an Elevation Certificate Lower Flood Insurance in Zone AE?

If you own a property in Flood Zone AE, you’ve probably heard that an elevation certificate can lower your flood insurance premium. In many cases, that’s true. But it’s important to understand that it does not guarantee savings for every property.

The real value of an elevation certificate comes down to one thing, whether the verified elevation data improves how your flood risk is being evaluated today. Understanding when it helps, and when it doesn’t, can prevent you from spending money unnecessarily.

Why Elevation Matters in Flood Zone AE

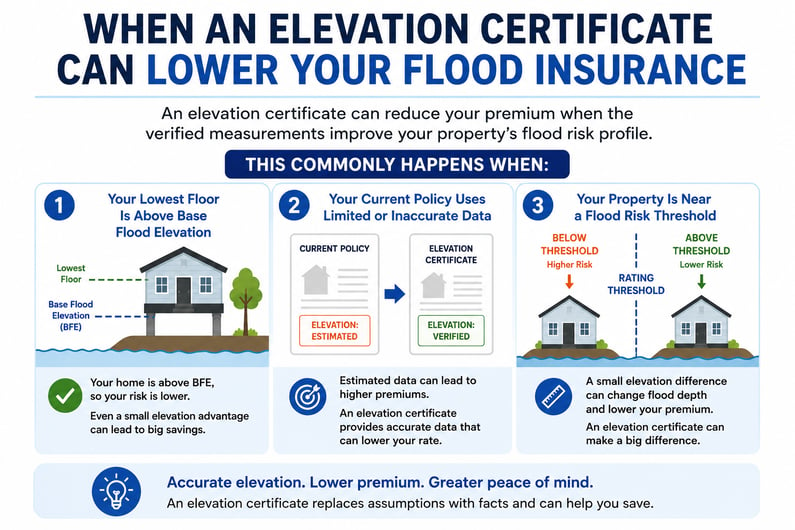

Flood Zone AE is considered a high-risk flood zone by FEMA. These areas have a defined Base Flood Elevation, also known as BFE, which represents the estimated height floodwaters could reach during a major flood event.

Generally speaking:

- Homes elevated above BFE are considered lower risk

- Homes below BFE are considered higher risk

- Even a difference of one or two feet can significantly impact premiums

Without accurate elevation data, insurance companies may rely on conservative assumptions when calculating your premium. Those assumptions can sometimes lead to higher rates than necessary.

That’s where an elevation certificate can help.

What Is an Elevation Certificate?

An elevation certificate is an official document prepared by a licensed surveyor, engineer, or architect that verifies important details about your property, including:

- The elevation of your lowest floor

- The Base Flood Elevation for your property

- Building characteristics

- Flood zone information

This document gives insurers precise measurements instead of estimates or outdated records.

Is an Elevation Certificate Worth the Cost?

Most homeowners want to know whether the savings justify the upfront expense.

In many markets, an elevation certificate costs around $800 as a one-time expense.

A simple way to evaluate the return on investment is to compare the expected annual savings to the upfront cost.

Rule of Thumb

If projected savings are at least $600 to $800 annually, an elevation certificate is often worth pursuing.

When an Elevation Certificate May NOT Be Worth It

Not every property benefits from elevation verification.

In some situations, existing survey data already indicates the home is negatively elevated compared to BFE. That means the property sits below the expected flood level.

When this happens, an elevation certificate may not improve the premium enough to justify the cost.

Instead, homeowners may achieve better savings by:

- Comparing private flood insurance options

- Reviewing replacement cost estimates

- Adjusting deductibles

- Reassessing coverage structure

Elevation vs. Shopping for the Cheapest Flood Insurance

Many homeowners search for the cheapest flood insurance policy possible. While comparing carriers is important, focusing only on the lowest premium can create long-term problems.

Some carriers offer aggressive introductory pricing that may increase substantially later.

An elevation certificate, on the other hand, improves the underlying risk profile of the property. That can create more stable savings over time rather than temporary discounts. For many Zone AE homeowners, improving the property’s rating accuracy is one of the most effective long-term cost reduction strategies available.

Frequently Asked Questions

Does an elevation certificate lower flood insurance in Zone AE?

Often, yes. If your home’s lowest floor is above Base Flood Elevation, verified elevation data can lower premiums by replacing conservative assumptions with measured data.

How much can an elevation certificate save on flood insurance?

Savings vary significantly. Some homeowners save little or nothing, while others save more than $3,000 annually depending on elevation differences and current policy assumptions.

When is an elevation certificate worth it?

It is usually worth considering when projected savings are at least $600 to $800 per year and the one-time certificate cost is around $800.

Do private flood insurance companies use elevation certificates?

Yes. Many private flood insurers use elevation data when evaluating flood risk and calculating premiums, especially for higher-risk properties in Zone AE.

Looking Ahead

An elevation certificate can absolutely lower flood insurance premiums in Zone AE, but it is not a guaranteed solution for every property.

The key factor is whether the verified elevation data improves your property’s flood risk profile compared to the assumptions currently being used by the insurer. Before spending money on an elevation certificate, it’s important to evaluate the likely impact first.

We can help estimate potential elevation savings, review replacement costs, and compare private flood insurance options to help you make an informed decision. Click below to access our free guide to elevation certificates.

Information contained on this page is provided by an independent third-party content provider. This website make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact editor @producerpress.com