Compare Flood Insurance Policies: A Comprehensive 7-Step Guide

Are you trying to decide between NFIP and private flood insurance, but not sure which one actually protects your property better?

You are not alone, and more importantly, you are not wrong to question it. Flood insurance is often misunderstood as a standardized product, but in reality, it varies significantly depending on the source.

In this guide, you will learn how NFIP and private flood insurance truly compare, how to evaluate quotes using real property data, what most homeowners misunderstand about deductibles, and how to choose a policy that actually protects you long term.

Step 1: Understand What You Are Actually Comparing

Before you ever look at price, you need to understand the product itself.

The National Flood Insurance Program, also known as NFIP, is backed by the federal government and administered by FEMA. It uses standardized pricing under Risk Rating 2.0 and is universally accepted by mortgage lenders.

Private flood insurance, on the other hand, is offered by individual insurance companies. Each carrier has its own underwriting rules, pricing models, and coverage options.

The key difference is this, you are not comparing two similar policies, you are comparing two completely different approaches to risk.

Step 2: Why Coverage Matters More Than Price

A lower premium does not mean better protection. In fact, it can sometimes mean the opposite.

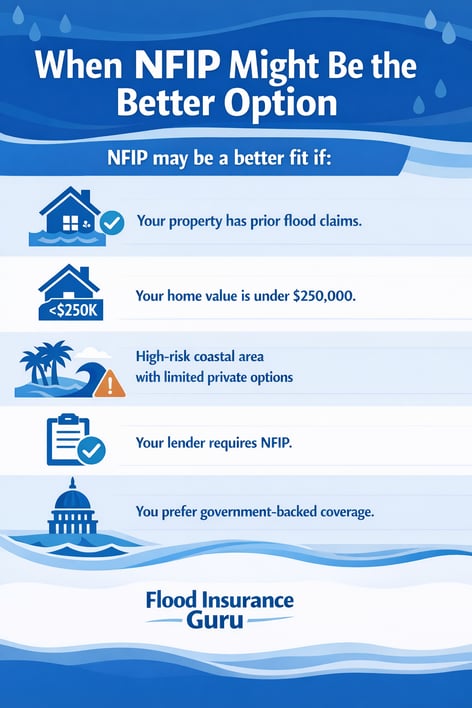

If your home costs more than $250,000 to rebuild, relying on NFIP alone may leave a significant gap in protection.

Step 3: Use Real Property Data, Not Estimates

Flood insurance pricing is highly specific to your property.

Key factors include:

- Elevation

- Flood zone

- Foundation type

- First floor height

- Distance to water

At Flood Insurance Guru, we have placed over 2,400 policies nationwide, with an average premium of $1,210 per year .

In many Zone AE scenarios, NFIP premiums can range from $2,000 to $3,000 or more. Meanwhile, private flood insurance can sometimes come in significantly lower.

In one real example, an NFIP policy was quoted at $2,899 annually, while a private policy for the same property came in at $327.

The takeaway is simple, estimates are misleading, real quotes are the only way to make an informed decision.

Step 4: The Truth About Deductibles

Many homeowners believe increasing their deductible will significantly lower their premium.

With NFIP, that is rarely the case.

For example:

- Increasing a deductible from $1,000 to $5,000 may only reduce your premium by about 2.5 percent

- On a $2,000 premium, that is roughly $50 in savings

You are taking on thousands in additional risk for minimal savings.

Private flood insurance works differently. Deductibles can have a more noticeable impact, sometimes saving a few hundred dollars annually depending on the carrier.

Step 5: Timing and Waiting Periods Matter

Flood insurance is not something you can wait to purchase.

- NFIP policies have a standard 30-day waiting period

- Private policies typically have 10 to 14-day waiting periods

- Some private carriers allow near immediate coverage in certain cases

Step 6: What Lenders Actually Require

If you have a mortgage, your flood insurance must meet lender requirements.

NFIP is always accepted.

Private flood insurance is also accepted in most cases, but it must meet federal compliance standards:

- Issued by an approved carrier

- Coverage equal to or better than NFIP

- Cannot be canceled mid-term without proper notice

Step 7: Think Beyond Today’s Price

The cheapest policy today is not always the best decision long term.

NFIP policies are currently increasing under Risk Rating 2.0, often by 15 to 18 percent annually until they reach full risk pricing.

Private carriers also adjust rates, but pricing is typically more closely tied to property-specific risk factors.

Before choosing a policy, ask:

- Has the NFIP rate reached full risk pricing yet?

- How stable is the private carrier?

- What is the carrier’s financial rating?

- Are there renewal caps or restrictions?

The best agents recommend the right solution, not just the cheapest one.

Frequently Asked Questions

Is private flood insurance accepted by lenders?

Yes, in most cases. The policy must meet federal compliance standards. If there is resistance, request a formal compliance review.

Can I switch from NFIP to private flood insurance?

Yes, switching at renewal is the easiest option. Mid-term changes are possible, but may involve partial premium loss.

Are private flood policies always cheaper?

No. While they are often more competitive, pricing depends on the specific property. The only way to know is to compare real quotes.

Why are NFIP premiums increasing?

NFIP pricing is being updated under Risk Rating 2.0 to reflect true flood risk, which often results in gradual annual increases.

Compare Smarter, Not Faster

Choosing between NFIP and private flood insurance can feel overwhelming, especially when the pricing and coverage look so different.

The problem was never just price, it was understanding what you were actually buying.

Your next step is to get real quotes from both NFIP and private carriers and evaluate them side by side based on coverage, cost, and long-term stability.

At Flood Insurance Guru, this is exactly what we do every day. We help homeowners and investors make informed decisions that protect their property and their finances.

Click below to take action and find the right policy for your situation.

Information contained on this page is provided by an independent third-party content provider. This website make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact editor @producerpress.com